Introducing Thematic Insights

Discover curated insights into emerging investment trends and themes. Our thematic approach provides valuable information to help you stay ahead of the market.

Interested in learning more about metals and mining companies?

See what investors are saying on the Stockhouse bullboards.

Stockhouse is the leading source of authoritative breaking stock market news for self-directed investors. Our team of markets reporters, editors and technologists cover the entire listed company universe in Canada. We cover over 3,985 businesses, their people, their investors and their customers. We write the stories that move Canadian capital markets. Along with Thematic Insights, Stockhouse reaches almost 2 million of the world’s most affluent and engaged investors each and every month. With an investor database of almost 600,000 subscribers and over 50 million monthly page impressions, Stockhouse is one of the fastest-growing business and finance platforms in the world.

Stockhouse's Thematic Investor Insights reports are a new way for investors to gain insight into global markets. With in-depth compelling research and data, Thematic Insights gives investors the big picture and provides context to the companies they are investing in.

The information in this report is for general use only and is not financial advice. This report does not take into account your personal financial situation or objectives. You should consult a qualified financial professional before making any investment. This report includes companies that have sponsored some parts of the report. All brands and trademarks included in this report remain the property of their owners.

®2024 Stockhouse Publishing Ltd. All Rights Reserved.

ANALYSIS AND INSIGHTS

Stay current with our latest Thematic Investor Insights report.

Sign up and subscribe today!

IN THIS REPORT

Interested in learning more about gold companies?

See what investors are saying on the Stockhouse bullboards.

The Hard Asset Century

A new economic era spells unprecedented opportunities in hard commodities

MARKET ANALYSIS

By Jeff Nielson, Business writer and analyst

October 2, 2024 | 20 minute read

Thematic Insights – Listen to the report

Stockhouse and The Market Online jointly present our latest Thematic Insights investor report, drawing from nearly 30 years of experience in delivering comprehensive information to the investor community, driving global economic trends. Our platform fosters a diverse investor community, facilitating informed decision-making through education, research, and dialogue. Our reports offer accessible education, essential financial tools, and the opportunity to engage in meaningful discussions on market complexities. We are committed to providing insightful analysis that transcends conventional metrics, believing in the importance of understanding underlying trends, industries, and innovations to empower informed investment choices.

The Future of Energy

Navigating our future economic needs and climate change goals will require a balanced approach relying upon nuclear power, oil & gas, and renewable energy.

An old era ends, and a new era begins

A new economic era driven by unprecedented demand for tangible commodities

OVERVIEW

What is the “Hard Asset Century”? It is nothing less than a new economic era into which the global economy is emerging.

It is replacing the Century of Paper – the 20th century – as a new-and-opposite economic paradigm.

Imagine a world where the demand for hard commodities – metals, minerals and fossil fuels – soars to unprecedented levels. Calculate the investment opportunities with the companies that find and produce these hard commodities: mining stocks.

Now factor in that these mining stocks have literally never been more undervalued in history, further amplifying potential returns. Not merely a once-in-a-lifetime opportunity, but a once in history investment opportunity.

For investors, this is what the Hard Asset Century represents.

The “financialization” of the global economy, centred in the West, is running low on steam. Economic growth in the global economy is now ramping up in the East and South. Asia and Africa, in particular, are poised for unprecedented growth.

What has previously limited economic development across these huge land masses with equally huge populations? Many of these countries are land-locked nations.

Without access to the major corridors of trade – the oceans – economic development has been stunted in most of these countries. Now, finally, in the 21st century we see a major, new economic initiative, the largest in history, bringing vital transportation infrastructure to these continents.

The transportation infrastructure will allow these nations, many of which are rich in natural resources, to fully industrialize. The infrastructure and subsequent industrialization imply demand for hard commodities are tracking to be off the charts.

The 21st century is evolving into the Hard Asset Century. As the name suggests, this is a re-focus away from financial assets and “financial products” back towards hard assets – with tangible value.

It is the re-emergence of “the real economy,” a global economy where the foundation of growth and the foundation of value are derived from hard assets. Despite this, our myopic markets have discounted the companies that find and produce hard commodities more than ever before.

The 20th century did not begin as a “century of paper,” much like the 21st century has not begun as a hard asset century.

The early decades of the 21st century were distorted by two world wars, which generated a massive (but temporary) expansion of the Western industrial base. Indeed, because of this, many casual observers would argue there has been no “century” of paper assets at all.

Birth of Hard Asset Century = commodities mega-bull

CONCLUSION

The premise of this edition of Thematic Insights is that now is the time for investors to gravitate towards hard assets in their financial holdings. Indeed, some of the world’s most powerful financial institutions have already been stockpiling hard assets for several years.

Central banks around the world are currently gravitating towards gold. Central bank gold purchases have soared to the highest on record, with virtually a new record for gold purchases each year. These bankers are demonstrating a greater and greater preference for gold over their own paper.

Central banks manufacture the world’s fiat currencies.

If the people who manufactured Fords all started buying Toyotas, what model of car should you buy? If you currently owned a Ford, wouldn’t you want to sell it as soon as possible?

Gold is the vehicle for central banks (and governments) to gravitate towards hard assets and away from depreciating paper assets, especially their own currencies.

For retail and institutional investors, gold is only one of the vehicles in which to invest to capitalize on a new supercycle in commodities. A whole spectrum of metals and minerals markets is under-capitalized and poised for revival.

Damaged (or even broken) supply chains are the insurance that the new bull markets for these hard commodities will enjoy extremely extended runs. Even with a flat demand curve, repairing the supply chains in these hard commodity markets would require massive new investment – spread across many years.

Mining companies, who find, develop and produce these urgently needed hard commodities provide natural leverage to rising commodity prices. No matter how fast commodity prices rise, the profit margins of commodity producers rise faster.

Read our next Thematic Insights special update, where we will zero in on this opportunity in mining stocks: how and why mining stocks are the most efficient vehicles for resource investors, why the junior mining stocks provide superior returns in a bull market, and we take an up-to-the-minute review of opportunities in individual resource markets.

The Hard Asset Century is emerging as not only a new economic era but an investment opportunity in hard assets unlike anything seen in previous history. While many commodity markets have already taken off, the commodity producers are priced at unbelievable bargains across the board.

Commodity investors have had to wait (literally) half a century for a new mega-cycle in commodities to materialize. With a century or more of commodity investment opportunities ahead, it should be worth the wait.

Capturing Market Trends with Insightful Analysis

brought to you by: Stockhouse and The Market Online

The World Bank has 189 member countries, staff from 170+ nations, and offices in over 130 locations. It comprises five organizations, including the International Finance Corporation (IFC).

(Photo: Adobe Stock; By: Kristina Blokhin)

However, since the Bretton Woods agreement in 1944, the global economy has been dominated by a single, paper instrument: the U.S. dollar. Eighty years later, that dominance is no longer secured.

For investors, this is their cue to look away from financial investments and towards hard assets with real, tangible value. Discover how a Second Industrial Revolution (Belt and Road Initiative) will power the extraordinary opportunities in hard commodities – and mining stocks.

Stay ahead of the curve! Whether you’re a beginner or an experienced investor, sign up today and never miss a report.

By providing my email, I consent to receiving investment related emails from Stockhouse.

PODCAST

Unlock Gold and Energy Market Secrets:

Mid-Year Update with Jeff Neilson and Coreena Robertson – Expert Insights, Strategies, and Trends for Savvy Investors!

In This Report:

An old era ends, and a new era begins

Dawn of the Hard Asset Century

The NEW (and greatest?) commodity supercycle

Global network finance, trading, and telecommunication connectivity on earth.

(Photo: Adobe Stock; By: sorin; Generated with AI)

The NEW (and greatest?) commodity supercycle

How price suppression and broken supply chains created a crisis in metals markets

CHAPTER TWO

In the early years of the Hard Asset Century, the demand for hard commodities has just started to inch higher. So, why are we witnessing a “supply crisis” in different metals/minerals markets on an increasingly frequent basis?

Answer: Supply chains have been severely degraded and, in some cases, completely broken for many of these hard commodities.

The severe damage to these hard commodity supply chains is because of two principal causes.

“Central banks stand ready to lease gold in increasing quantities should the price rise.”

Dawn of the Hard Asset Century

Commodities poised for reversal amid global industrial transformation

CHAPTER ONE

We can see the coming of the Hard Asset Century from two perspectives. On the one hand, commodities have been mired at a 50-year low versus stocks.

Commodities to Equities Ratio.

(Source: IncrementumAG; Reference: Interactive Brokers, LLC; Copyright: 2019 Crescat Capital LLC;)

Commodities are due for a powerful reversal versus equities – and other paper assets. A new “industrial revolution” will drive this powerful reversal.

While hard assets will inevitably strengthen, paper assets (most notably the U.S. dollar itself) are rapidly weakening.

De-dollarization is now more than a mere economic trend. It is an irreversible and accelerating process.

The increasing weaponization of the U.S. dollar in the form of “economic sanctions” has created a global imperative to replace the dollar in international trade as rapidly as possible. Indeed, today roughly 40 per cent of the global population is being subjected to various U.S. economic sanctions.

The U.S. dollar is increasingly viewed as a toxic financial instrument.

In 2020, the U.S. dollar still accounted for 59 per cent of all foreign currency reserves. Today, less than four years later, that share has already plunged to 48.2 per cent.

59%

48.2%

2020

2024

25%

50%

75%

The most powerful argument that a Hard Asset Century is beginning is that much of the global economy is just beginning a massive industrial transformation.

- A global Second Industrial Revolution (Belt and Road Initiative) will require far more commodities and other manufacturing inputs than at any time in history, creating a premium for such hard assets.

- The global supply chains for many (most?) commodity markets have been severely degraded. As rising demand exposes these broken supply chains, the premiums on commodities and other hard assets will increase even further.

China’s BRI will transform the global economy

A Second Industrial Revolution? How else could we describe China’s “Belt and Road Initiative”?

Officially, roughly 150 nations have signed up to participate in the BRI, representing more than 60 per cent of the global population.

China’s “Belt and Road Initiative”, The construction of a BRI-funded railway in Purwakarta, Indonesia.

(Source: Getty Images; By: Xu Qin/Xinhua; Reference: Council on Foreign Relations)

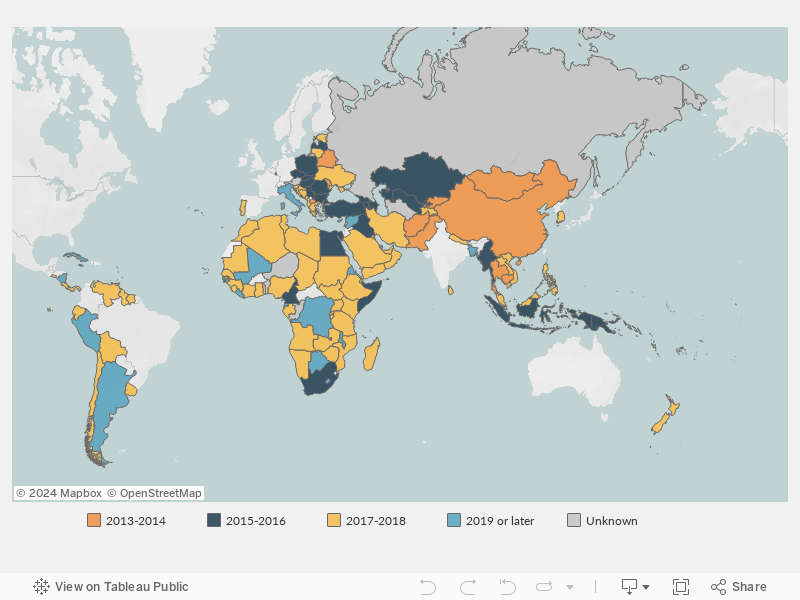

- The Belt and Road Initiative Has Gone Global, Official BRI participants by year of joining

- Source: https://www.cfr.org/backgrounder/chinas-massive-belt-and-road-initiative

The Belt and Road Initiative Has Gone Global

Official BRI participants by year of joining

Note: The publicly available information from countries marked as "unknown" is either unclear or contradictory.

(Source: Green Finance and Development Center; Green Belt and Road Initiative Center; Belt and Road Portal; Reference: Council on Foreign Relations)

The first Industrial Revolution, centred in Western nations, represented approximately 20 per cent of the global population. However, it would be a colossal mistake to estimate that the Second Industrial Revolution will “only” be three times as large as the original Industrial Revolution.

At the beginning of the Industrial Revolution, the global population was less than 1.5 billion people. This means the first Industrial Revolution represented massive economic growth for approximately 300 million people.

In contrast, the Second Industrial Revolution will represent massive economic growth for 5.1 billion people. That represents 17X as many people, and many more partially developed and under-developed nations might eventually participate in the BRI.

The Second Industrial Revolution (Belt and Road Initiative)

~300 million people participated in the Industrial Revolution

Over 5.1 billion people will participate in Second Industrial Revolution (BRI)

That’s ~17 times as many people

Yes, many of the approximately 150 BRI nations are already partially industrialized. But to fully industrialize more than 60 per cent of the planet up to the level of a 21st century modern economy is an economic project that will entirely dwarf the Industrial Revolution – by at least an order of magnitude.

Ten times as much infrastructure created. Ten times as much “stuff” manufactured. And (eventually) 10 times the demand for hard commodities to fuel this massive growth.

Already, more than $1 trillion has been invested in BRI-related projects. But this barely qualifies as “the tip of the iceberg.” Ultimately, tens of trillions of dollars will be invested to capitalize this global economic transformation.

The growth profile for this 60 per cent of the global population will be so large and so long that we can only speculate on when and where it will end. We are on the path towards at least a Hard Asset Century.

Broken commodity supply chains

Even if we currently had robust, abundant supply chains for all these hard commodities, this projected demand would/will represent a commodities boom that will stretch across (at least) a century. However, supply chains today are anything but “robust.”

In recent years, we have seen numerous major commodity markets (hard and soft commodities) spike to near-record or record-high prices in recent years because of some form of supply crisis.

TABLE: The NEW Commodity Supercycle (Brianna)

The NEW commodity supercycle

2018

Hard Commodity

Soft Commodity

2021

Lumber

Iron Ore

2022

Lithium

Soybeans

Coal

Aluminum

Oats

Wheat

Corn

2024

Copper

Cocoa

Yes, many of the hard and soft commodity markets above saw distortions in price partially because of the global shutdown during the COVID pandemic.

However, most of these same commodity markets saw previous spikes to record-highs during the peak of the last “commodity supercycle” in 2008 – when there were no exogenous forces affecting these markets.

The Second Industrial Revolution (Belt and Road Initiative)

What does it take to power an industrial revolution?

Capital. Labour. Raw materials.

With 5.1 billion people (including the youngest populations on the planet), there is a near-infinite supply of young, cheap labour available. This is in stark contrast to the aging societies of the West.

Capital? Let’s start with China.

In the original Industrial Revolution, capital formation occurred gradually and mostly organically. It was the profits of one phase of the Industrial Revolution that were used to fund the next stage of growth.

Today, measured in terms of purchasing power parity (PPP), China’s economy is now significantly larger than the United States’ – 25 per cent larger according to the most-recent estimate.

Imagine how much more powerful the growth cycle would have been for the Industrial Revolution if an economic powerhouse such as China already existed to capitalize that growth.

Yes, the first Industrial Revolution had the British Empire. But at the dawn of the Industrial Revolution, the population of England and Wales was only 8 million people. Scarcely comparable to the economic clout of China’s 1.4 billion people.

The capital necessary to fund the Second Industrial Revolution is plentiful, especially if we add the additional economic resources from the rest of the BRICS bloc.

By PPP, the BRICS 10 is now larger than the G7. That economic disparity would inevitably continue to grow, even without the approximately 50 additional nations already queueing up to join BRICS.

What is in short supply are raw materials: the hard commodities that will be needed to transform all this capital and labour into infrastructure, machinery and consumer goods.

As 5.1 billion people work to transform at least 60 per cent of the global economy, backed by many of the world’s largest economies, accurate projections for the amounts of these commodities that will be required (and used) are impossible.

This is a socioeconomic phenomenon in the overall development of humanity that is simply too large to grasp, let alone accurately estimate.

The Industrial Revolution began in 1760 and persisted for roughly a century. However, many historians point to a second half of this Industrial Revolution, where the original industrialized nations of the West (and, to a lesser extent, other parts of the world) modernized their industrial economies.

The second era of the Industrial Revolution, Women working machines at the American Woolen Company, Boston, c. 1912.

(Source: Britannica; Reference: Industrial Revolution)

This second period of growth/development includes everything from computerization and automation all the way to nanotechnology. This second era of industrialization has stretched across roughly an additional century.

In the Second Industrial Revolution driven by the BRI, all this technology has already been developed. This means watching countless nations evolve from agrarian societies to computerized, urbanized, and modernized societies – all in a single, extended trajectory of growth.

How long will this take, even aided with the speed of modern technologies? One century? Two centuries?

Referring to the dawn of this new economic era as the Hard Asset Century will likely prove to be conservative. It will be an era of mega-growth that will persist beyond even the extended lifespan of 21st century Homo sapiens.

Across these decades of enormous economic growth, we will see “commodity supercycles” come and go.

Commodity markets are inevitably volatile for a combination of reasons. Either supply or demand (or sometimes both) can be unstable in any individual commodity market. This implies cycles of under-supply (“booms”) and over-supply (“busts”).

In the case of hard commodities, this volatility is further exacerbated by the extended time required to significantly ramp up supply in response to a surge in demand.

It can easily require a decade to construct a mine to put a new ore deposit into commercial production. That time horizon is extended significantly if we also include the years required to find and develop that mineral resource.

Thus, under a best-case scenario, it would/will be an enormous challenge for the global mining industry to keep up with rapidly rising demand virtually across the full spectrum of metals and minerals.

However, what we currently face is anything but “a best-case scenario.” What we see in 2024 are broken supply chains becoming increasingly prevalent in many metals and minerals sectors.

For this reason, the first commodity supercycle of the Hard Asset Century may, in hindsight, prove to be the longest-and-strongest supercycle.

- Suppression of commodity prices has left major mining companies under-capitalized and unable to fund necessary mine maintenance, development and expansion.

- Suppression of mining stocks (especially the junior exploration companies) has resulted in most mining sectors being unable to fund any significant level of metal/mineral exploration.

The mechanisms for such price suppression are the Big Bank trading algorithms that now control more than 80 per cent of all market trading.

The motive for suppressing commodity markets is “fighting inflation.” Lower commodity prices mean lower prices for finished goods – and a lower “inflation” reading. In turn, this lower perceived inflation helps to hide the speed at which paper assets are losing their value in real dollars.

The evidence of this financial strategy is all around us, dating back at least 26 years.

– Testimony of Federal Reserve Chairman Alan Greenspan to the Committee on Banking and Financial Services, July 24, 1998

Gold “leasing” is a quasi-legitimate financial transaction where gold is “loaned” from official reserves so it can be dumped onto the market to suppress the price of gold.

Gold is universally known as the proverbial canary in the coal mine with respect to telegraphing inflation. Thus, gold was the first (and most important) target of the bankers in their commodity price suppression scheme.

Today, the poster child for hard commodity markets that have been undermined through this financial suppression is copper.

How badly has the copper industry been hurt through the “inflation fighting” of the Big Banks? Just ask Goldman Sachs analysts who wrote a recent note:

“The combination of record low copper stocks [globally], our expectation of peak mine supply next year, rapid green demand growth, and low price elasticity of both demand and supply will in our view lead to copper scarcity pricing in 2025.”

Copper, Commodity price trends in industrial metals, shaped by supply and demand dynamics and economic growth.

(Photo: Adobe Stock; By: supansa; Generated with AI)

Let’s dissect this piece by piece.

Despite the fact that S&P Global is projecting that global copper demand will double by 2035, copper mine supply is projected to “peak” in 2025.

Why is it that copper mining companies who could soon sell (potentially) twice as much copper will be unable to increase supply at all, starting next year?

The world’s major copper producers have been unable to fund necessary mine maintenance, development and expansion because of low copper prices. Mine reserves have declined dramatically. Copper grades and margins are steadily falling.

Major copper producers have been unable to fund necessary mine maintenance, development and expansion due to low copper prices

Mine reserves have declined dramatically

Copper grades (and margins) are steadily falling

$10s of billions in new capital needed TODAY to make up for decades of under-investment

Production falling for some of the world’s largest copper producers

These major producers need to find tens of billions of dollars in new capital – today – to catch up with all these years of under-investment. Some of these major producers require billions in new investment just to prevent their copper production from declining precipitously.

We need look no further than the world’s largest copper producer, Codelco.

From January 29, 2024:

Chile’s state-owned miner sold two tranches of debt worth a total of $2 billion last week at 230 basis points and 235 points above U.S. Treasuries, a wider spread than on its existing notes…

Codelco needs the money after embarking on a $40 billion spending program following decades of underinvestment.

From April 26, 2024:

Top copper producer Codelco reported a decline in quarterly output due to lower quality ore at its aging Chilean mines — the latest sign of supply-side struggles that have helped send metal prices to two-year highs.

Think this is an anomaly?

In December 2023, Anglo American reduced its “copper guidance” for 2024 by 200,000 tonnes, and it is projecting a further decline in copper production in 2025 – despite this major bull market.

This is the good news in the copper mining industry. If you want to see the real “scorched earth” from Big Bank financial suppression, look at the catastrophe in copper exploration, as pointed out by mining icon Robert Friedland, founder and Co-Chairman of Ivanhoe Mines (TSX:IVN).

Table/Chart: Copper discoveries (Brianna)

Copper discoveries 1990-2021

Major discoveries per calendar year

(Sources: Robert Friedland, S&P Market Intelligence @synergyrescap

Previously, the copper mining industry consistently produced six to 15 “major discoveries” of new copper deposits per year.

Copper remains abundant in the Earth’s crust. So, why have major copper discoveries declined by 98 per cent over the past decade?

Let’s ask Goldman Sachs.

Let’s translate that headline in the context of the copper mining industry today.

The share prices of junior copper exploration companies have been suppressed to less than 10 per cent of any reasonable fair market value. Thus, they are able to fund less than 10 per cent of the exploration in which they would otherwise be engaged.

What do you get from that? A 98 per cent decline in major copper discoveries during a “supercycle” for copper.

Goldman Sachs cynically calls this “an underinvested supercycle.”

Today, despite the price of copper recently hitting an all-time high (and with further price increases on the horizon), most junior copper exploration stocks are trading near or at all-time lows. And this comes at a time of “record low copper stocks” [inventories].

Copper supply is flat. Copper inventories are at record-lows.

Copper demand is projected to double. And virtually zero major copper deposits are in the long-term supply pipeline.

- Descriptive graphic/text graphic Title: Broken copper supply chain (Brianna)

- Copper supply is flat

- Copper inventories at record low

- Copper demand projected to double

- Major copper discoveries have declined by 98% over the past decade

Broken copper supply chain

Yet the only companies in the world that can find more badly needed copper are trading at all-time lows and are thus unable to fund any significant level of copper exploration.

It’s not only Stockhouse that sees an enormous opportunity when these copper stocks break free from this financial suppression.

This is the opinion of one renowned international commodities trader.

That’s roughly quadruple the recent record-high for the price of copper.

- [long-term copper chart + projected price increase] (Brianna)

- Title: Price of copper (past and projected)

- Chart copper prices: https://tradingeconomics.com/commodity/copper

- Monthly copper price data: https://ycharts.com/indicators/copper_spot_price

Global price of copper, 1990 - 2024

Chart copper prices (Sources: Trading Economics, Copper) | Monthly copper price data: (Sources: YCharts, Copper Spot Price)

If copper itself is projected to quadruple from its recent record price and copper demand is projected to double, the companies that find-and-produce copper should already be trading at all-time highs.

This is the worst supply crisis in the history of the copper mining industry. It comes in the early stages of a major commodity supercycle that will (ultimately) play out over a span of decades.

Today, the “supply crisis” is in copper. Tomorrow, the crisis could be in silver or lithium or nickel, or some other major metals market.

All mining stocks have been subjected to this same Big Bank price suppression over the past decade. All mining sectors are thus having their supply chains severely degraded.

Each metals market is different.

Some metals markets have flatter demand profiles and/or deeper supply chains. But sooner or later – barring an end to mining stock price suppression – every one of these metals and minerals markets is going to experience the same scorched-earth supply crisis.

Will silver be the next metal to enter a once-in-a-lifetime supply crisis? Are we already there? We certainly seem to be headed in that direction.

The Silver Institute expects significant deficits will persist for years. In fact, the cumulative total deficits of 2021, 2022 and 2023 are approximately 474Moz, which is nearly 50 per cent of 2023’s total supply.

Huge supply deficits for silver. And this is nothing new for the silver market. Silver has faced a perennial supply deficit for most of the past 30 years.

This pending supply crisis comes at a time when silver is historically undervalued. Indeed, large, persistent supply deficits are the strongest indicator of under-pricing.

Among the New Age metals of the 21st century economy, supplying enough lithium for the battery industry appears problematic. But here the supply challenges are more operations oriented.

Even with the “game-changing technology” of direct lithium extraction, attempting to extract sufficient lithium from brine resources is doubtful because of the severe water constraints that characterize brine geography.

Increasing lithium production from lithium-rich clay formations is one answer. These lithium clay deposits are amenable to even more-efficient extraction methods.

A lot of lithium is also potentially available in hard-rock lithium deposits (spodumene). However, most such deposits face high capital and operating costs.

The price of lithium would have to be sustained at a much higher level than the current price for a lot of this hard-rock lithium to get to market. And lithium stocks would have to be priced near/at fair-market levels to finance this development.

Uranium has already entered a new, long-term mega-bull market.

- [graphic: price of uranium, projected increase in nuclear?] (Brianna)

Title: The uranium mega-bull market

- Chart of past uranium prices from 2000 + “Nuclear power projected to double by 2050” with upward sloping dotted ling

- Monthly uranium price data: https://ycharts.com/indicators/uranium_spot_price

Global price of uranium, 2000 – 2024

Monthly uranium price data: (Sources: YCharts, Uranium Spot Price)

Nuclear power generation is projected to double over the coming decades. Climate change activists have (reluctantly) acknowledged that emissions-free nuclear power is part of the climate change solution – not part of the problem.

Investors can see this guaranteed increased demand for uranium for many years to come. Thus, major uranium producers have enjoyed new all-time highs in their share prices. Even some of the junior exploration companies have had good runs.

As the “mega-bull” opportunities in other metals markets become increasingly obvious, one by one we will see the revaluation of mining stocks (much higher) in additional metals/minerals markets.

Could anything derail the Belt and Road Initiative (Second Industrial Revolution) and thus shrink this source of projected demand for hard commodities?

Yes. Unfortunately, we currently see two horrific military conflicts raging in the world – in locations of extreme geopolitical importance.

Even worse, both of these military conflicts are very unstable. In Israel and Ukraine, we are hearing an increasing clamour of the risk of (literally) World War III.

Wars are disruptive. World wars are obviously the most disruptive.

However, as we pointed out at the beginning of this edition of Thematic Insights, fighting a world war requires a very large base of heavy industry. Such heavy industries are voracious consumers of hard commodities.

If (worst case) we should spiral into a world war – and humanity doesn’t get wiped out in a nuclear conflagration – the supply of hard commodities will likely be disrupted more than the demand. Thus, a worst-case war scenario could easily result in even more-lucrative investment opportunities in metals markets.

Copper is used profusely throughout the military supply chain. If World War III erupts, copper could hit $100,000 per tonne.

Why central banks and savvy investors are rushing to hard commodities

Investment Highlights

- Anfield Energy is focused on consolidated assets in the Uravan Mineral Belt split between Colorado and Utah

- The company’s Shootaring Canyon Mill is one of only three licensed, permitted and constructed uranium mills in the United States

- It boasts strong fundamentals for uranium and vanadium with a focus on domestic U.S. developers and producers

Anfield Energy is a Vancouver, B.C.-based uranium and vanadium development and near-term production company with key assets including the Shootaring Canyon Mill in Garfield County, Utah, and the Slick Rock Project in San Miguel County, Colorado.

The Shootaring Canyon Mill is strategically located within key uranium production areas in the United States and is one of only three licensed, permitted and constructed uranium mills in the country.

The mill began operations in 1982 but ceased operations after six months. The mill produced and sold 27,825 pounds of uranium.

Anfield Energy acquired a 100 per cent interest in the mill from Uranium One in 2015. The conventional acid leach facility is also licensed to produce up to 750 tons of ore per day.

The company’s other priority program is the Slick Rock Project, which covers approximately 5,333 acres with 315 contiguous mineral lode claims. The project is ideally located in an apparent intersection of two major mineral trends along the Uravan Mineral Belt.

In 2023, a preliminary economic assessment was completed that unveiled a Slick Rock-attributed estimated inferred mineral resource of 7.7 million pounds of uranium oxide with an average grade of 0.224 per cent, along with 47.1 million pounds of vanadium oxide with an average grade of 1.35 per cent.

Future Outlook

Because the Shootaring Canyon Mill has largely been dormant and thanks to its acquisition of the mill, the focus of Anfield Energy will be getting it up and running again in the near to long term.

Corey Dias, CEO

“We have seen significant technical advancement with regard to our assets over the last few months: the submittal of the mill restart application in April; submittal of a Plan of Ops for the Velvet-Wood mine in May; receipt of approval for a drill program at Slick Rock in June; now, confirmation of the completeness review of the mill restart application.”

TSXV:AEC, OTC:ANLDF

Anfield Energy Inc.

CEO: Corey Dias | Market Cap: $66.21 million

Canadian Companies in Commodities

Small-Cap stars in the Hard Asset Boom

By Jocelyn Aspa, Markets Reports, Stockhouse and The Market Online

October 1, 2024 | 7 minute read

With the rise of hard assets and commodities reaching new heights, investors have no shortage of options to choose from in terms of companies making an impact in the space.

Below are four small-cap companies trading on Canadian exchanges that have projects in development as well near and long-term goals investors can look forward to.

Investment Highlights

- The company has three core projects that include lithium-hard-rock pegmatites across Canada and Ireland

- Its primary focus is on the Raleigh Lake hard rock lithium and rubidium project in Ontario

- International Lithium is focused on increasing shareholder value by advancing its core projects at the appropriate stages

With its headquarters in Vancouver, B.C., International Lithium is primarily focused on lithium exploration properties in Canada and Ireland. Its primary strategic focus is on the 48,500-hectare Raleigh Lake lithium and rubidium project near Ignace, Ontario, and it’s seeking strategic opportunities in Zimbabwe.

At Raleigh Lake, a preliminary economic assessment was published in December 2023 and reported an after-tax net present value of C$342.9 million and an after-tax internal rate of return of 44.3 per cent per annum.

In addition to its focus at Raleigh Lake, International Lithium also has the highly prospective Firesteel Copper Project in Ontario under its belt, which it officially acquired in May 2024.

The company acquired a 90 per cent interest in the Firesteel Copper Project, which is a highly prospective grassroots copper and cobalt property.

International Lithium previously completed a 1,392 line-kilometre airborne magnetic and electromagnetic survey using its RESOLVE frequency domain electromagnetic system. The data will be interpreted to identify near-surface highly conductive zones that may represent massive sulphide mineralization consisting of pyrrhotite, chalcopyrite, pyrite and bornite.

Future Outlook

In the near-to-long-term, International Lithium will continue its path towards development at Raleigh Lake as well as advancing towards the first drilling program at Firesteel targeting copper mineralization.

Jon Wisbey, CEO

“Firesteel is primarily a copper project. Initial studies reveal highly prospective amounts of copper at Firesteel, and there is also a smaller amount of cobalt and some gold there, too. Exposure to copper fits our battery metals strategy well and is geographically a very natural follow-on for ILC from our investment in 2022 in the nearby Wolf Ridge claims.”

TSXV:ILC, OTC:ILHMF

International Lithium Corp.

CEO: John Wisbey | Market Cap: $4.7 million

Investment Highlights

- The company holds the past-producing, high-grade Argosy Gold Mine in the prolific Red Lake District of northwestern Ontario, which has significant depth potential

- The adjacent North Birch Project offers additional blue-sky potential

- Pinnacle Silver and Gold intends to target future acquisitions in Mexico, Peru and the United States

Pinnacle Silver and Gold has its headquarters in Vancouver, B.C., and is currently focused on two highly prospective gold projects in the Red Lake Mining Division of northwestern Ontario, including the past-producing, high-grade Argosy Gold Mine, which is open to depth, and the adjacent North Birch Project that offers district-scale discovery potential.

Both projects are within 10-12 kilometres of the Springpole Gold Deposit, which is being developed by First Mining Gold (TSX:FF).

The company is primarily focused on the Argosy Gold Mine, which sits within the northern part of the Birch-Uchi Greenstone Belt of the Superior Province of the Precambrian Shield. The Birch-Uchi Belt lies between the prolific Red Lake and Pickle Lake Greenstone Belts and contains similar geology.

Previous activity at Argosy took place between 1931 and 1952 and produced 101,875 ounces of gold and minor amounts of silver from 276,573 tons of ore at an average grade of 0.37 ounces per ton (12.7 g/t) gold. The property then lay dormant until 1974 and has been minimally explored since.

Pinnacle is also actively looking for other district-scale opportunities in the Americas, with a particular focus on silver and gold.

Future Outlook

In the coming months, Pinnacle Silver and Gold aims to begin drilling at the Ontario projects and initiate project acquisitions across the Americas.

Bob Archer, CEO

“With the gold price hitting new highs and silver rising faster, this is a great time to be exploring, making new discoveries and building companies. Not only do our Red Lake properties present an opportunity to do that but the downturn the last few years has resulted in acquisition opportunities through which we intend to grow the company.”

TSXV:PINN, OTC:NRGOF

Pinnacle Silver and Gold Corp.

CEO: Bob Archer | Market Cap: $1.22 million

Investment Highlights

- Boasts a portfolio of three projects spanning 59,057 hectares in Antioquia, Colombia’s premier mining district

- Is drill-ready and has a strategic partnership in place for 10,000 metres of drilling

- Has a tightly held share structure with management and board holding 65 per cent

Quimbaya Gold is based out of Vancouver, B.C., and is focused on the exploration and acquisition of mining properties in Antioquia, Colombia.

It is primarily focused on the Tahami Project in the Segovia region of Colombia. The project spans an area of 17,087 hectares and is surrounded by established operations, including Aris Mining, Somas Gold, Mineros, Soma Gold Corp. and Sun Valley.

In August 2024, the company revealed a strategic partnership with Independence Drilling S.A. of Colombia for 100,000 metres of drilling.

The company will execute drilling campaigns with a minimum of 1,500 metres each. Drilling is expected to begin over the course of Q3 2024 and will assist the company in proving the potential existence of gold mineralization in its properties.

The company wouldn’t be able to advance the drilling campaigns without the backing of its management and advisory board. In other words, a project – no matter its potential – holds no value without an experienced team.

Case in point, Quimbaya Gold’s team, including CEO Alexandre P. Boivin, has more than a decade of experience in Colombian mining as well as Juan Pablo Bayona, executive chairman, who has raised more than US$1 billion in capital as head of Barings for Colombia and Peru.

Additionally, Pietro JL Solari, director, secretary, and Dr. Stewart Redwood, consulting geologist, bring vital experience and skill to the team.

Future Outlook

With Quimbaya Gold’s primary focus on the Tahami project and its 100,000-metre drilling campaign, the company will begin drilling, complete drilling and get assay results in the near- to long-term.

Pietro JL Solari, Head of Investor Relations

“Through Quimbaya Gold, you get exposure to one of the largest underexplored high-grade mining districts in the world, at a current valuation below $C15 million.”

CSE: QIM, OTCQB: QIMGF

Quimbaya Gold

CEO: Alexandre P. Boivin | Market Cap: $13.43 million

Total currency reserves including gold

Collapse of the global copper supply chain

Sign up and stay up to date with upcoming news from the companies that interest you most!

By providing my email, I consent to receiving investment related emails from Anfield Energy, International Lithium, Pinnacle Silver and Gold, Quimbaya Gold and Stockhouse.